Of all the cloud companies in the industry today, Alphabet’s Google is the one company that had the longest and strongest experience in managing large scale data center infrastructure. But alas, it was the last company to join the Infrastructure-as-a-Service race with its Google Compute Engine.

Note: Cloud reviews for AWS, Microsoft, IBM and Oracle are linked near the bottom of this article.

Google’s bread and butter is its search engine, and the company has built many conduits like Android, Google Chrome and Google Maps to keep traffic flowing towards it search engine.

Google’s mission is to organize the world’s information and make it universally accessible and useful; and in order to achieve that mission Google has to archive everything that it comes across on the web, which is exploding with data with each passing day. Google has been doing this since the time it was founded, and their success till now is a clear indication that they are experts in managing IT infrastructure at massive scale.

What should have been their biggest strength, however, also turned out to be their biggest weakness. Google is one company that can keep running itself out of capacity as its needs constantly keep rising unlike any other company.

Nevertheless, they had solid technology expertise in running their own datacenters, and the company has now realized that staying out of the cloud game would end up damaging their business prospects in the long run, because two other technology giants were slowly getting ahead on several fronts.

It was the right decision, but one that came a little too late. Alphabet does not break out its cloud revenues simply because it is much smaller than Microsoft’s and Amazon’s revenues from their cloud businesses. As it stands, very few people inside the company actually know how fast Google Cloud Platform has grown, and it will remain that way till GCP reaches comparable scale.

One of the most important decisions the company made once it decided that it was time to kickstart their cloud infrastructure push was the hiring of Diane Greene, co-founder of VMWare, to run the unit. They also brought Google for Work (now GSuite), GCP, Google Apps and all other cloud-based services under her control.

In and of itself, that was a smart move because it really doesn’t make sense to keep IaaS separate from SaaS and PaaS.

But that wasn’t enough.

Google also realized that it needed a much larger datacenter footprint. Compared to what Amazon and Microsoft had, Google’s datacenters for cloud were a much smaller asset.

Take Europe, for example. Google has data centers in St. Ghislain, Belgium, while Amazon already has footholds in Ireland, Frankfurt and London, and IBM has data centers in Netherlands, Germany, Italy, France and the United Kingdom, and is expecting to add Sweden and Norway to the list soon.

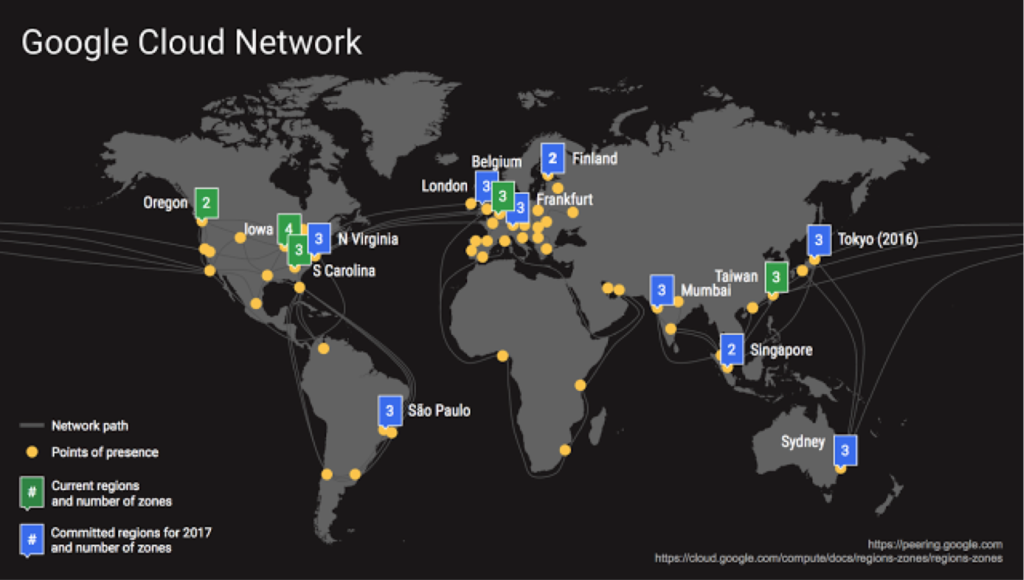

A datacenter and its network play a crucial role in IT infrastructure management and, as of now, Google starts way behind the curve with respect to the current segment leaders. Google knew this, and moved to address this issue at the earliest. The company announced in its blog post early last year that it will be adding ten additional Google Cloud Platform regions before the end of 2017.

“To meet this growing demand, we’ve reached an exciting turning point in our geographic expansion efforts. Today, we announced the locations of eight new Google Cloud Regions — Mumbai, Singapore, Sydney, Northern Virginia, São Paulo, London, Finland and Frankfurt — and there are more regions to be announced next year.

By expanding to new regions, we deliver higher performance to customers. In fact, our recent expansion in Oregon resulted in up to 80% improvement in latency for customers. We look forward to welcoming customers to our new Cloud Regions as they become publicly available throughout 2017.” – September, 2016 Google Blog

As you can see, an expansion of the network will play a huge role in reducing latency for customers.

In the meantime, Amazon and Microsoft will keep reducing the cost of their offerings, adding even more pressure on Google to keep its own pricing as close as it can to them – or, if possible, to go even lower than them.

But pricing is not even an issue here because Google is never going to face a shortage of funds as long as their core ad revenues keep growing at double-digit rates, which they have consistently been doing.

To put it in a nutshell, Google has the strength because it already has the talent in place, but it lacks the infrastructure and services stack that it needs to compete with the leaders of the segment.

It will take a few more years for the company to get into a position from where it can pose a serious threat to Amazon or Microsoft, but with billions of dollars in cash Google has the pocket that can keep it in the hunt for a really long time. Until then, it will be all about acquisitions to bolster its services, expansion of data centers and signing up big ticket clients.

It’s a slow road to the top, but Google cannot afford to sit back and watch. Microsoft is a huge threat lurking around the corner. The company has its own search engine, a better office productivity suite and is growing extremely fast in the cloud segment.

As more and more companies gravitate towards Microsoft, it will make the company a one-stop provider of SaaS-PaaS and Iaas, and put a huge lid on Google’s ambitions in the office productivity space where it has positioned its GSuite.

Google’s hurdles are high and numerous, and it will take a sustained effort from Diane Greene’s team as well as continued support from top management for the company to make a dent in the cloud computing industry – whether that’s in IaaS, PaaS or SaaS.

ALSO READ:

Cloud Industry Review 2016 Part 1: Amazon Web Services (AWS) Growth

Cloud Industry Review 2016 Part 2: Microsoft Cloud Growth

Cloud Industry Review 2016 Part 3: IBM Cloud Growth

Cloud Industry Review 2016 Part 4: Oracle Cloud Growth

Thanks for reading our work! We invite you to check out our Essentials of Cloud Computing page, which covers the basics of cloud computing, its components, various deployment models, historical, current and forecast data for the cloud computing industry, and even a glossary of cloud computing terms.