The global device market is not even in a state of flux, it is already in a state of saturation. The PC market has already declined for five years in a row, and is well on its way to make it an even six. The smartphone market is growing, but only in certain parts of the world. Wearables offered brief hope, but they still remain a big hype. And now, the tablet market has also joined the race to move lower and lower.

AI-powered smart speakers are slowly moving the needle, but the potential market size cannot be as big as the smartphone market, and device manufacturers around the world are now left scrambling for ideas to make sure that are able to survive the new market conditions – flat growth, low margins and high competition.

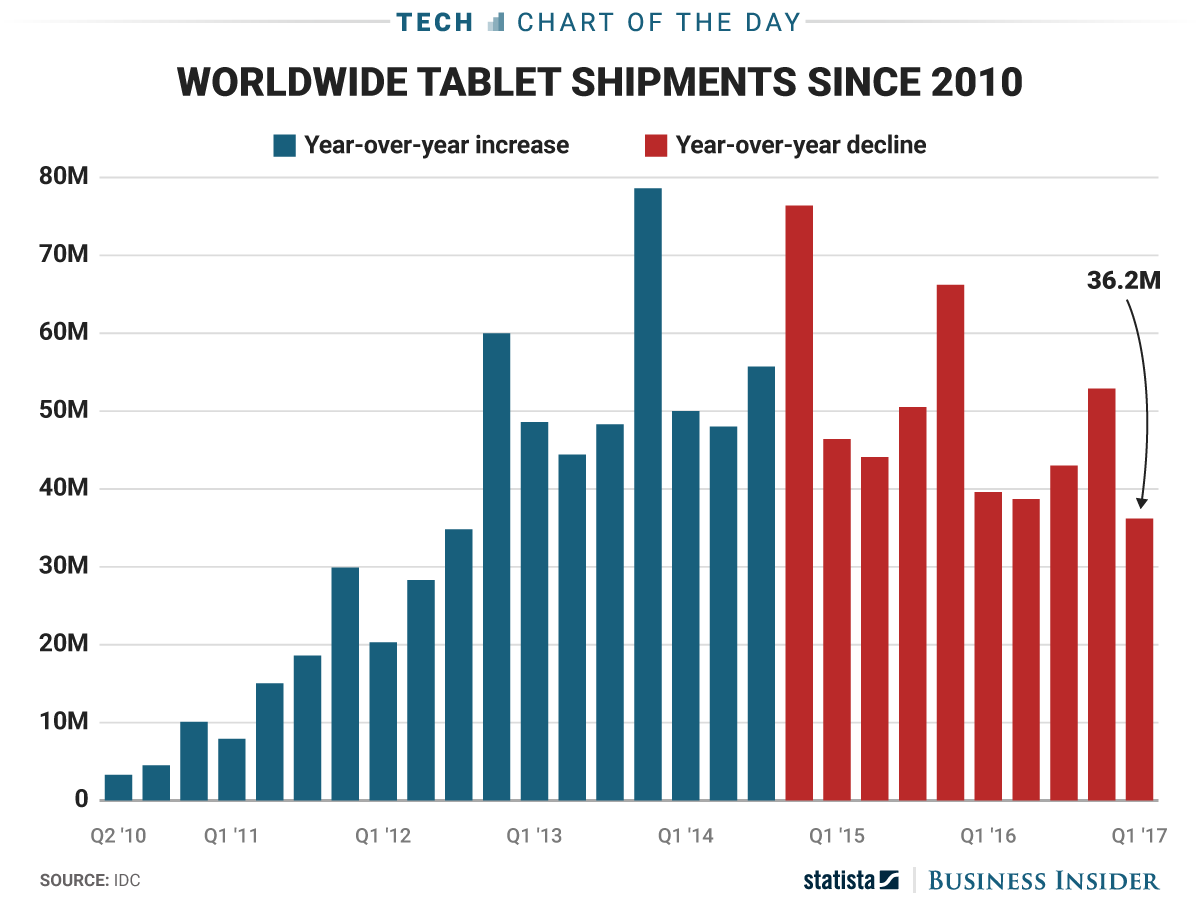

According to IDC, one of the world’s leading market research firms, global tablet shipments reached 36.2 million during the first quarter of 2017, a decline of 8.5% compared to last year, making it the tenth consecutive quarterly decline.

The research firm also noted that detachable tablets are trouncing regular tablets that lack keyboards.

“A long-term threat to the overall PC market lies in how the market ultimately settles on the detachable versus convertible debate,” said Linn Huang, research director, Devices & Displays at IDC. “To date, detachable shipments have dwarfed those of convertibles, but growth of the former has slowed a bit. In IDC’s 2017 U.S. Consumer PCD Survey, fielded over the previous two months, detachable owners held slightly more favorable attitudes towards their detachables than convertible owners did for their convertibles. However, owners of both were far more likely to recommend a convertible over a detachable.”

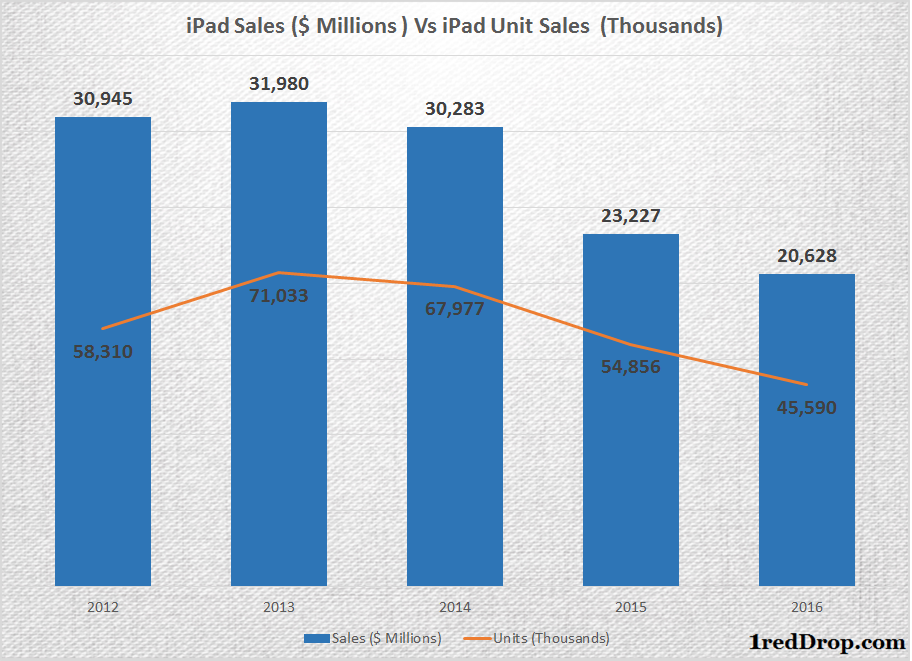

Apple is still the number one player in the tablet market. As a premium player, it was able to buck the sharp declining trends faced by other manufacturers. Now, however, things are starting to move in the other direction for the company across all its product lines. The newly launched iPhone, for example, helped Apple record massive sales during the first quarter, only to see its unit sales numbers slip by 1% during the second quarter of the current fiscal.

Tablet sales have now been on the decline for 13 consecutive quarters. Global tablet sales have been declining since early 2015, and IDC’s outlook for tablets is certainly not good news for Apple. In the first six months of the current fiscal, Apple sold 22.003 million iPads compared to 26.373 million units last year, a decline of 17%.

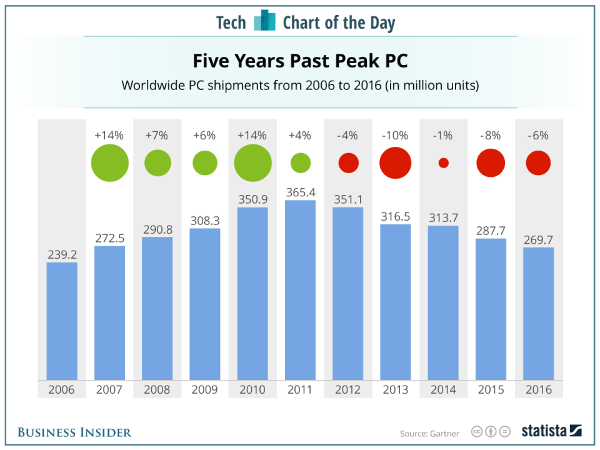

The biggest surprise during the first quarter – on the devices front – was the PC market, which kind of stopped its downward momentum, posting near flat growth of 0.6%. But it is far too early to make the call that we have found the bottom of the PC market.

If consumers are buying detachable tablets, it negates the need to buy PCs as well, not just tablets. Moreover, PCs will also have to fight smartphones before they can get into households. The odds of a person upgrading their smartphone is much higher than the odds of a PC upgrade.

We still need PCs for our work, and commercial is where PCs can really shine because they will win that market fair and square against smartphones and tablets. But that market is much smaller than the consumer PC market. The PC market has improved its numbers, and it may have arrested the decline for now, but it would be too early to start expecting an upward trend in this segment.

That leaves us to the much larger smartphone market to think about. Apple created the market literally out of nowhere, and it was a common sight to see double-digit smartphone sales growth during the 2009-2014 period. But there are only so many hands around the world we can push smartphones into. Every person added to the smartphone pool is one person less in the potential smartphone market.

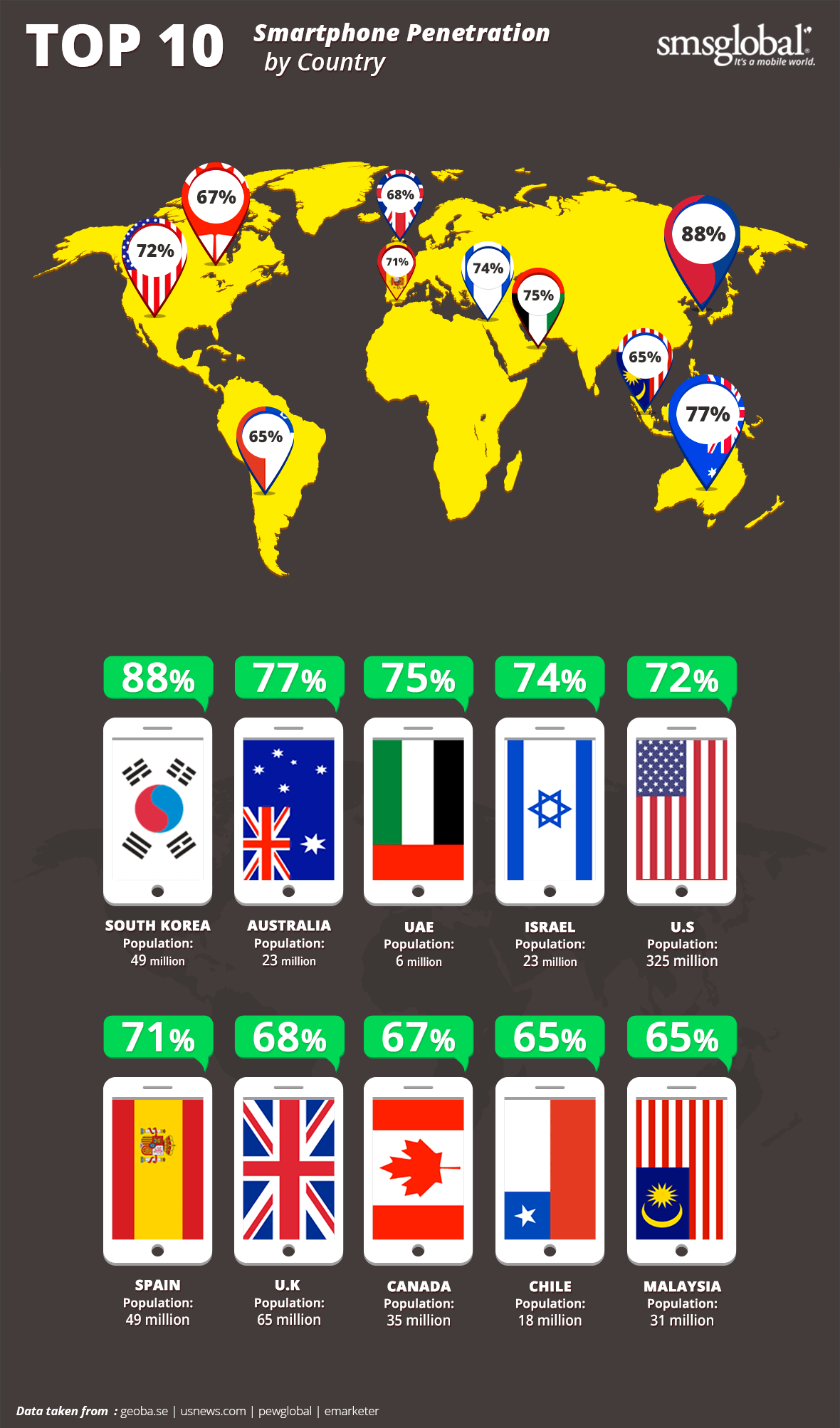

As you can see from the chart above, smartphone penetration in major developed countries are well above 70%. In other words, nearly seven out of ten people already have a smartphone in their hand. Selling a smartphone to some one who already uses a smartphone is not the same as selling it to some one who didn’t have one to begin with. And that’s the essence of the challenge faced by smartphone makers today.

Thankfully, this is a problem restricted to developed markets, and also the reason why sales are more robust in developing countries. But with that shift comes another problem – pricing and margins. So, it’s not really a surprise to see IDC forecast single-digit growth numbers for this segment overall, over the course of the next few years.

“The worldwide smartphone market will reach a total of 1.5 billion units shipped in 2016, up 5.7% from the 1.4 billion units shipped in 2015. From there, shipments will reach 1.92 billion units in 2020, the final year of our forecast period, resulting in a CAGR of 6.0%.”

“As smartphone penetration continues to escalate in many regions across the globe, 2015 likely represents the last year of double-digit (10.4% over 2014) smartphone growth that we will see,” says Anthony Scarsella, research manager for IDC’s Mobile Phones team.

“Despite the overall single-digit growth we expect over the forecast period, there still exist many promising high-growth markets for vendors to attack over the coming years.

“Markets such as Indonesia, India, Africa, and the Middle East will present great opportunity for vendors to push.

“Mature markets such as the United States, China, and Western Europe will need to rely heavily on selling frequent upgrades to existing customers to maintain market share. New trade-in plans and leasing options set in place by both carriers and vendors such as Apple are the first vital step to ensure stability and continued growth.”

Though IDC seems to be pointing at opportunities in the smartphone market, things are never going to be the same for companies like Samsung, Apple and Google. The days of growth are long gone, and they need to gear up to handle a highly mature, stable-growth and highly competitive device market, with very little margin for error. Ups and downs will now become a common sight: the weaker ones will fold, making way for bigger, stronger companies with high staying power.

As operators in the premium segment, Apple and Samsung have profitable smartphone units, which will allow them to survive the new state of the smartphone market. It will be an extremely difficult period to navigate in the short term, but the ones that survive will stay for a really long time.

Thanks for visiting! Would you do us a favor? If you think it’s worth a few seconds, please like our Facebook page and follow us on Twitter. It would mean a lot to us. Thank you.