IBM’s journey of transformation has been a long and arduous one, and is far from being over. Big Blue has now watched over 20 consecutive quarters of revenue decline and, looking at the 3 percent rate at which revenues declined during the most recent quarter, it’s clear that IBM needs several more quarters to get things back on the growth path.

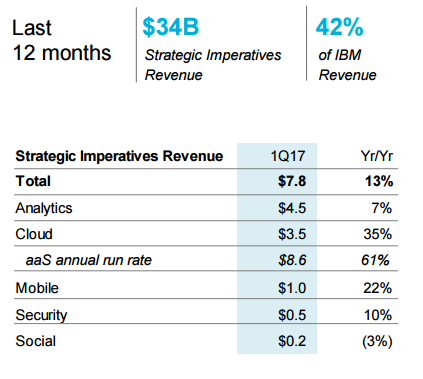

IBM did make a conscious decision to dive into forward-looking business segments such as analytics, cloud, security and so on – business segments that typically have high operating margins, and which could serve the company well for decades. The biggest hurdle, however, is that these business lines, which IBM calls its Strategic Imperatives, still account for only 42% of their overall revenues.

Revenues from strategic imperatives increased by $800 million during the most recent quarter compared to last year, but IBM’s net revenue declined by $529 million during the same period. Clearly, IBM’s legacy revenue streams are losing ground much faster than growing revenue streams are able to gain it.

On the positive side, this trend will make sure that strategic imperatives will account for the bulk of Big Blue’s revenues much soon than if things had been otherwise. Once it hits that critical point, IBM can then focus solely on growing revenues from forward-looking businesses, without having to worry about legacy units dragging down their growth numbers quarter after quarter.

Unfortunately, Warren Buffett recently threw a big spanner in the works by announcing that he has trimmed down his position. He’s still kept two-thirds of his IBM holding, but when Warren makes a move in any direction, a chunk of the market is bound to mirror that move.

This is what he had to say about his decision:

Buffett, who owned about 81 million shares of IBM at the end of 2016, sold off about a third of that stake in the first and second quarters of 2017. As he told CNBC:

“I think if you look back at what they were projecting and how they thought the business would develop I would say what they’ve run into is some pretty tough competitors,” Buffett said. “IBM is a big strong company, but they’ve got big strong competitors too.”

What Buffett is talking about is the way the competition is shaping up in the cloud computing industry, and the more recent impact of the Software as a Service segment. Six years ago, there were only Amazon, Microsoft and IBM fighting for space in the fast-growing industry focused primarily on cloud infrastructure in all its forms. Today, we have Oracle and Google in the race as well, and they’re all companies with plenty of talent and deep pockets.

In an earlier article, we spoke about how Microsoft has effectively dragged its competitors towards the SaaS segment, where IBM still plays a niche role with its analytics unit. Hybrid cloud is on the way up, and this is where IBM is particularly strong, but other players are not going to sit by and watch if enterprises around the world start embracing hybrid in a big way. And with all of them now attacking the SaaS market, it could lead clients to the competition if IBM has nothing to match their capabilities, service for service.

So, yes, the landscape has indeed changed drastically over the last five years, like Buffett says, and could offer even stronger headwinds against IBM’s strategic imperatives’ growth in the coming quarters.

Can IBM ride the storm that’s already brewing in the cloud computing horizon? Will things have to get worse before they can get better? That remains to be seen. The company is most definitely headed in the right direction with its forward-looking units, but it is now a question of a carefully orchestrated effort involving multiple parts – marketing, sales, portfolio expansion, depth of offering, and the deliberate choice to focus on hybrid solutions.

Thanks for visiting! Would you do us a favor? If you think it’s worth a few seconds, please like our Facebook page and follow us on Twitter. It would mean a lot to us. Thank you.